We’ve had some weird weather around here this year. First, there was the record-breaking cold in January/February. More recently, we’ve had wild oscillations in temperature: 80s one week, 30s the next. And the weather across the US (and in many parts of the world) has been unusual as well.

It could just be a patch of random weather that won’t repeat. But it could also be that our climate is changing, and we can expect more of this. We’ll see.

One industry that isn’t waiting to find out is the insurance industry. It has already been taking steps based on projections that indicate that we probably have some serious changes coming.

In Florida and in California, insurance companies have been charging higher premiums or just refusing to cover buildings that are insufficiently resistant to risks such as wildfires and hurricanes. This has forced people who can’t upgrade to the level required by private insurers to turn to the state-run FAIR (Fair Access to Insurance Requirements) plans.

In California, the FAIR plan ran out of money in the wake of the LA fires, which meant taxpayers had to pick up the tab to the tune of around 1 billion dollars. That hasn’t happened yet to Florida’s FAIR plan, but it surely could. Florida doesn’t require insurance companies to show sufficient capital reserves to handle severe hurricane losses, and that means smaller insurers could be bankrupted by a major storm. In that case, taxpayers are likely to be stuck with the bill.

Some people simply can’t find an affordable way to insure their homes. Some of them are starting to leave the parts of Florida and California that are most threatened. They’re looking to settle in places where climate change is less of a problem.

Florida and California are not exceptional. Similar problems exist in many other states. If you want a more detailed picture of the situation, you can read The Uninsurable Future, published in 2025 in the Yale Law Journal Forum. This 56-page document is written by Dave Jones, the former Insurance Commissioner for the State of California, and it provides a comprehensive view of the problem, including information on where people are now moving.

For more details on people’s movements in response to climate change, check out the recent book “On the Move: The overheating earth and the uprooting of America” by Abrahm Lustgarten. It shows in great detail the ways in which climate is dislocating people and the places they are moving to. And of course, those migrations will grow rapidly in coming years in response to climate change. One example: the number of northern retirees moving to Florida is now countered by an equal number moving in the opposite direction, ending a 100-year trend.

But does it happen here? Here at Kendal, we don’t have the sinking coastlines of Florida, the tinderbox hillsides of California, nor the blistering heat of Arizona. Must we be concerned about insurability and climate change in our area?

It is true that our problems are currently less severe than those areas, and getting insurance probably won’t be a problem. In decades past, we had local flooding problems on our campus from runoff in big storms, but aggressive storm-sewer work has eliminated that, at least for now. We have not had droughts severe enough to lead to wildfire threats in our area (although southern New Jersey and parts of Pennsylvania have experienced wildfires and forest fires).

Yes, it happens here. Still, we mustn’t get complacent. We aren’t immune to weather issues. Here are two examples.

In 2014, we had a severe snowstorm that closed the roads and took down a lot of power lines. Kendal was without power from the grid for more than 24 hours, and our supply of diesel fuel for the big generator ran out. Our cottages and part of the Center were without power for half a day, until a diesel delivery truck could get through. Fortunately, the smaller generator that supplies the healthcare area still had fuel and continued running. Will another equally severe snowstorm happen again some year? Probably.

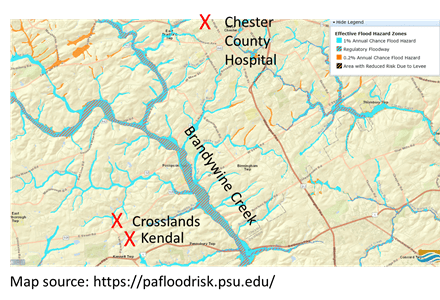

Or consider the floods on the Brandywine. Every few years, the Brandywine floods sufficiently to close the crossings at routes 1, 926, and 82. When that happens, Chester County Hospital is inaccessible in case of an emergency. Fortunately, Christiana Care (outside of Wilmington) is likely to still be reachable, but it’s a much longer drive.

It doesn’t seem likely that those two hazards will have much of an impact on our insurance rates. But rates in general will be rising as insurance companies seek to protect themselves against catastrophic losses.

What can be done? In The Uninsurable Future, Dave Jones offers some suggestions for what insurers might do. Two of them are things we might consider working on ourselves.

- Require insurers to divest from fossil fuels. It’s crazy, but insurance companies still have large investments in fossil fuels. We need to push for regulations that prohibit insurance companies from making these investments.

- Require reduced premiums for customers that mitigate climate-related risks. Did Kendal get a break on its premiums when it dealt with the stormwater runoff problem? It should have. If we make a significant move toward local solar and batteries, that too should qualify for an insurance break.

Regardless of the local details, the big story here is that insurance companies are really starting to take climate change seriously. They have to, if they want to stay in business in a period of sudden shifts in the weather and increased periods of both drought and precipitation. Climate change will entail a lot of costs, and that will show up in insurance premiums before most of us are hit with the more direct costs.